Travel insurance is not simply protection against a canceled flight. For a trip to South Korea, the most important coverage is usually emergency medical treatment, medical evacuation, trip interruption, and assistance when you cannot communicate easily with a hospital or service provider.

Most short-term tourists are not covered by South Korea's National Health Insurance Service (NHIS). Requirements can also differ for students, working-holiday participants, and other long-term visitors. Check both your immigration status and the exact wording of your insurance policy before departure.

Information in this guide was verified on June 9, 2026. Insurance conditions, visa rules, and assistance services can change.

Quick answer

- Buy insurance as soon as you make non-refundable bookings if you want cancellation protection.

- Choose medical coverage large enough to handle hospitalization and, if necessary, transport to another country.

- Confirm that South Korea is included in the policy's geographical area.

- Declare pre-existing medical conditions as required by the insurer.

- Check exclusions for hiking, skiing, motorcycling, alcohol-related incidents, and paid work.

- Save the insurer's 24-hour assistance number and policy details offline.

- In a medical emergency in Korea, call 119. For police, call 112.

- Keep medical records, receipts, prescriptions, police reports, and transport documents for a claim.

Is travel insurance required to enter South Korea?

There is no single insurance rule covering every foreign visitor. Requirements depend on nationality, visa category, purpose of stay, and the Korean diplomatic mission handling an application. Use the official Korea Visa Portal and confirm requirements with the Korean embassy or consulate responsible for your place of residence.

Insurance can be a formal visa condition in some cases. For example, the official Korea Working Holiday guide states that applicants need appropriate health insurance for their stay and lists minimum medical coverage of KRW 40,000,000. Conditions may vary by nationality and diplomatic mission, so working-holiday applicants should not rely on a general tourist checklist.

Even when insurance is not an entry requirement, traveling without it means accepting the financial risk of treatment, an early return home, canceled bookings, and lost property.

Why medical coverage matters in Korea

South Korea has an extensive healthcare system, but access to a hospital does not mean treatment is free. Short-term visitors generally do not receive the benefits available to enrolled NHIS members.

The NHIS guidance for foreigners explains that many registered foreign residents become subject to Korean health insurance after living in the country for more than six months, while employees at covered workplaces may be enrolled through employment. These rules are intended for qualifying residents, not ordinary short-stay tourists.

International travelers should therefore be prepared to pay medical charges themselves unless a hospital accepts a payment guarantee from their insurer. Payment procedures vary by hospital and policy. Ask your insurer whether it can arrange direct billing or whether you must pay first and request reimbursement later.

Korea does not have one fixed visitor price for a consultation, scan, emergency-room visit, or hospital stay. Charges depend on the facility, treatment, and whether services fall outside Korean national insurance benefits. Avoid policies with medical limits that would cover only minor outpatient treatment.

What a useful policy should cover

Emergency medical treatment

Look for coverage for illness, accidents, hospitalization, diagnostic tests, surgery, prescribed medicine, and emergency dental treatment. Read the benefit limits rather than relying on labels such as comprehensive or premium.

Check these details:

- Is outpatient treatment covered as well as hospitalization?

- Is there a deductible or excess for every visit?

- Must you contact the insurer before treatment?

- Are private and university hospitals eligible?

- Does the policy cover prescribed medicine after discharge?

- Are COVID-19 and other infectious diseases treated like other illnesses?

- Are pregnancy-related emergencies covered, and until what stage?

A requirement to obtain prior approval should not delay urgent care. In an emergency, seek help first and contact the insurer as soon as reasonably possible.

Medical evacuation and repatriation

Medical evacuation covers medically necessary transport when suitable treatment is unavailable locally. Repatriation can cover an approved return to your home country for treatment. These benefits are separate from the cost of an ordinary flight change.

Check who decides whether evacuation is medically necessary. Insurers commonly require approval from their assistance team and consultation with the treating doctor. A traveler who independently purchases a business-class flight or private medical transport may not be reimbursed.

Also check for repatriation of remains and reasonable travel or accommodation expenses for a companion if you are hospitalized.

Trip cancellation and interruption

Cancellation coverage normally applies only to specified events, not a general change of mind. Covered reasons may include serious illness, bereavement, major damage to your home, or certain transport disruptions.

Review whether the policy covers:

- Non-refundable flights and accommodation

- Prepaid rail passes, tours, or attraction tickets

- Additional accommodation after a covered disruption

- An early flight home after a family emergency

- Missed connections caused by an insured delay

Buy the policy soon after making major bookings. Events already known when you purchase insurance are usually excluded.

Baggage, electronics, and documents

Check both the overall baggage limit and the per-item limit. The per-item limit is especially important if you carry a laptop, camera, tablet, or expensive phone. Some policies require valuables to remain in hand luggage and exclude unattended property.

For lost property in Korea, report the loss promptly to the transport operator, hotel, airline, or police as appropriate. Korea's National Police Agency operates the official LOST112 lost-property service. An insurer may require a written loss report rather than a screenshot showing that you searched for the item.

Passport loss is usually covered under travel-document benefits rather than ordinary baggage coverage. Contact your embassy or consulate in Korea for replacement procedures.

Personal liability

Personal-liability coverage may help if you accidentally injure someone or damage their property. Confirm whether it applies to rented accommodation, bicycles, sports, and accidental damage to another person's belongings.

Liability insurance is not a substitute for vehicle insurance. If you rent a car, read the rental company's collision, deductible, third-party, tire, glass, and roadside-assistance conditions separately.

Activities that need extra attention

Standard policies may exclude activities considered hazardous. Check the exact activity list if your itinerary includes:

- Hiking in national parks or on winter trails

- Skiing or snowboarding

- Scuba diving or other water sports

- Cycling tours

- Paragliding

- Driving a scooter or motorcycle

- Competitive sports or organized races

For motorcycling, coverage may depend on engine size, licensing, helmet use, and local law. Personal medical coverage also does not remove your obligation to hold legally required vehicle insurance.

Paid work, internships, volunteering, and study can fall outside a leisure policy. Exchange students should check their university's insurance requirements and whether the school plan covers travel outside campus, semester breaks, mental healthcare, and repatriation. Working-holiday travelers need a policy compatible with both employment and visa conditions.

Common exclusions to read carefully

Policy exclusions matter more than the marketing summary. Pay particular attention to:

- Undeclared pre-existing conditions

- Treatment that can reasonably wait until you return home

- Routine checkups and elective treatment

- Incidents involving alcohol or illegal drugs

- Reckless or illegal conduct

- Unattended baggage

- Travel against medical or government advice

- Natural disasters already known before purchase

- Claims without supporting documents

- One-way travel or trips longer than the policy's maximum duration

Do not assume a credit card's complimentary insurance is sufficient. Activation may require paying for part or all of the trip with that card. Medical limits, trip-length limits, age restrictions, and coverage for additional cardholders can also differ.

How to choose a policy step by step

1. Define the whole trip

Use the dates from the day you leave home until the day you return, including stopovers. List every destination if Korea is part of a multi-country itinerary.

2. Calculate prepaid costs

Add up the non-refundable portions of flights, hotels, tours, rail bookings, and events. Your cancellation limit should reflect the amount you could actually lose.

3. Identify medical risks

Consider existing conditions, prescription medicines, pregnancy, age, planned activities, and whether you will visit islands or remote mountain areas.

4. Compare benefit limits and exclusions

Compare policies using the full policy wording. Check medical treatment, evacuation, cancellation, baggage per-item limits, deductibles, and exclusions on the same page or spreadsheet.

5. Check the claims process

Find out whether claims can be submitted online, what documents are required, and how quickly an incident must be reported. Confirm that the emergency assistance line works from South Korea.

6. Save evidence before departure

Store the policy certificate, policy wording, purchase receipt, emergency number, and claim instructions offline. Leave a copy with a trusted contact.

What to do if you need medical help in Korea

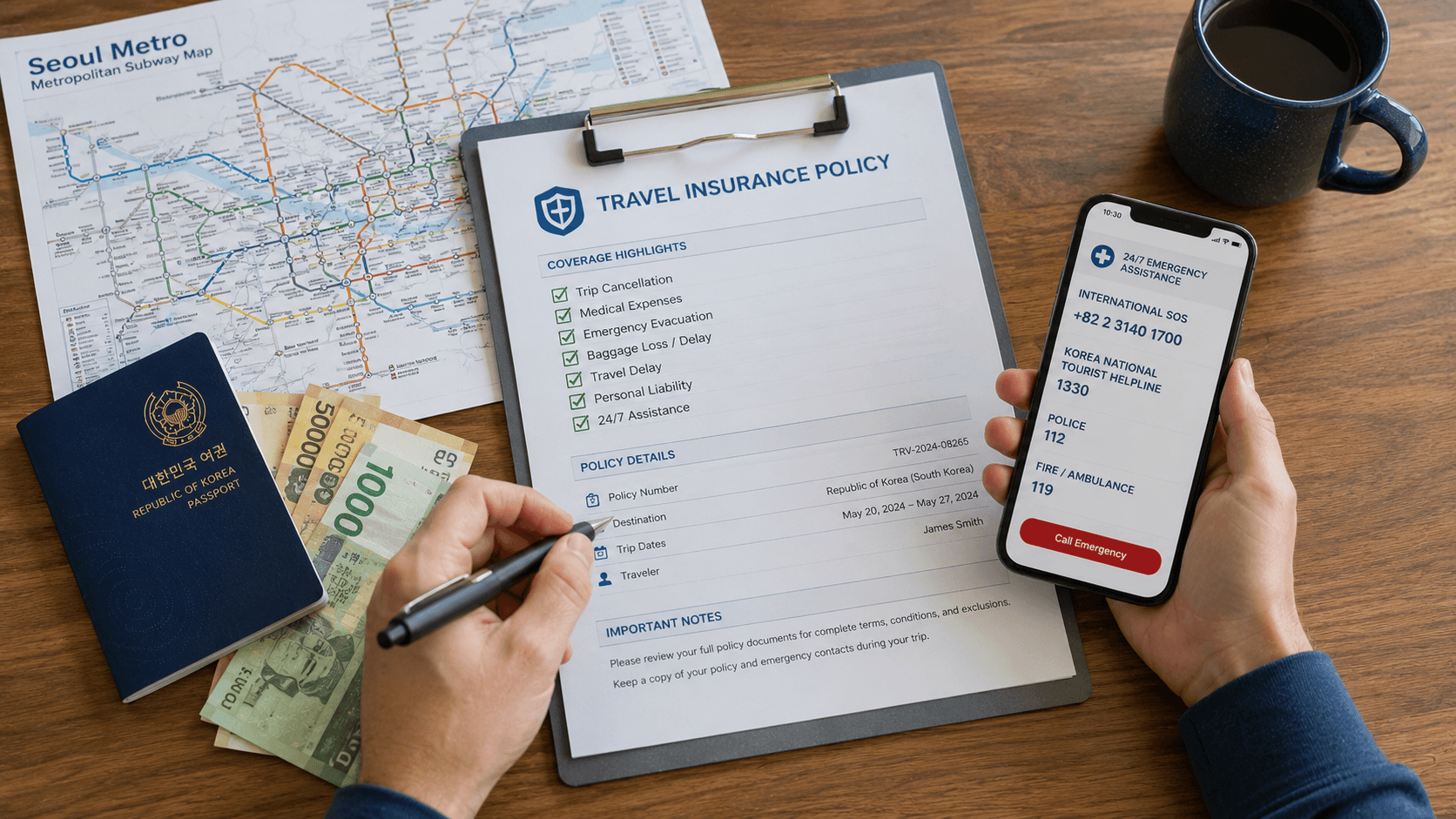

For a serious accident, fire, rescue situation, or medical emergency, call 119 without an area code. The Korea Tourism Organization's official emergency information lists 112 for police, 119 for fire and medical emergencies, and 1339 for infectious-disease inquiries. These numbers were verified on June 9, 2026.

For non-emergency tourism assistance and interpretation, call the 1330 Korea Travel Hotline. Language availability is listed on the same official emergency-information page.

For nearby emergency facilities, consult the government-operated E-Gen National Emergency Medical Center. Confirm opening hours directly, particularly at night and during Seollal or Chuseok holidays.

When possible:

- Take your passport or another accepted identification document.

- Call your insurer's assistance service.

- Ask whether the insurer can issue a payment guarantee.

- Show the hospital your policy certificate, but expect that you may still need to pay.

- Request an itemized bill, receipt, medical report, diagnosis, and prescription.

- Keep receipts from pharmacies and transport to the hospital.

- Ask for documents in English if available, but do not assume every facility can provide them immediately.

Large hospitals may have international healthcare centers, but services and operating hours vary. The government-supported Medical Korea directory can help identify registered institutions serving international patients.

Making an insurance claim

Notify the insurer promptly, especially for hospitalization, evacuation, trip interruption, theft, or expensive property loss. Record the claim reference number and the name of the assistance representative.

Useful evidence can include:

- Booking confirmations and proof of payment

- Written cancellation or delay notices

- Medical reports and itemized invoices

- Pharmacy prescriptions and receipts

- Police or lost-property reports

- Photographs of damage

- Airline baggage reports

- Proof of ownership for valuable items

- Records of calls or messages with the insurer

Keep the original documents until the claim is settled. If a document is issued only in Korean, ask the insurer whether a translation is required before paying for one yourself.

What to check before you go

- Confirm that the policy covers South Korea and your complete travel dates.

- Verify any insurance condition attached to your visa or study program.

- Declare relevant medical conditions accurately.

- Check coverage for every planned sport or activity.

- Review deductibles and medical, cancellation, and per-item limits.

- Confirm the procedure for direct hospital billing.

- Download the policy and emergency contacts for offline access.

- Carry enough available credit or emergency funds for upfront expenses.

- Pack prescription medicine in its original packaging with supporting documentation where appropriate.

- Give your itinerary and insurance details to a trusted contact.

FAQ

Can I buy travel insurance after arriving in Korea?

Some insurers allow this, but waiting periods, reduced benefits, or residency restrictions may apply. You cannot normally insure an event that has already happened or was already foreseeable. Buying before departure is usually more practical.

Does Korean National Health Insurance cover tourists?

Ordinary short-term tourists are generally not NHIS members. Foreign residents may become eligible or subject to mandatory enrollment depending on employment, immigration status, and length of stay. Long-term residents should confirm their position directly with the National Health Insurance Service.

Will a Korean hospital bill my insurer directly?

Possibly, but do not assume so. Direct billing depends on the hospital, insurer, assistance provider, and treatment. Call the insurer as early as possible and be prepared to pay and claim reimbursement.

Is travel insurance included with my credit card?

It may be, but eligibility and benefits depend on the card agreement. Check activation rules, covered travelers, trip duration, medical limits, exclusions, and whether the card includes evacuation rather than only accident benefits.

Sources

- Korea Visa Portal

- Korea Working Holiday entry requirements

- National Health Insurance Service guidance for foreigners

- VISITKOREA emergency information

- National Emergency Medical Center

- Medical Korea registered-institution information

- National Police Agency LOST112

Before purchasing a policy, compare its full wording against your itinerary and confirm any visa-specific requirement with the Korean diplomatic mission handling your application.